What is GIFT City / GIFT IFSC & IBU — in brief

- GIFT City is a special financial zone in Gujarat, India, developed to be the country’s first International Financial Services Centre (IFSC).

- Within GIFT City, banks (Indian and foreign) set up dedicated branches known as IFSC Banking Units (IBUs). These IBUs operate under a special regulatory regime governed by the International Financial Services Centres Authority (IFSCA), separate from regular domestic banking.

- For clients (especially Non-Resident Indians — NRIs), IBUs in GIFT IFSC offer the ability to hold bank accounts and deposits in foreign currencies (not Indian Rupees).

What is “GIFT City USD FD” (or Foreign-Currency FD via GIFT City)

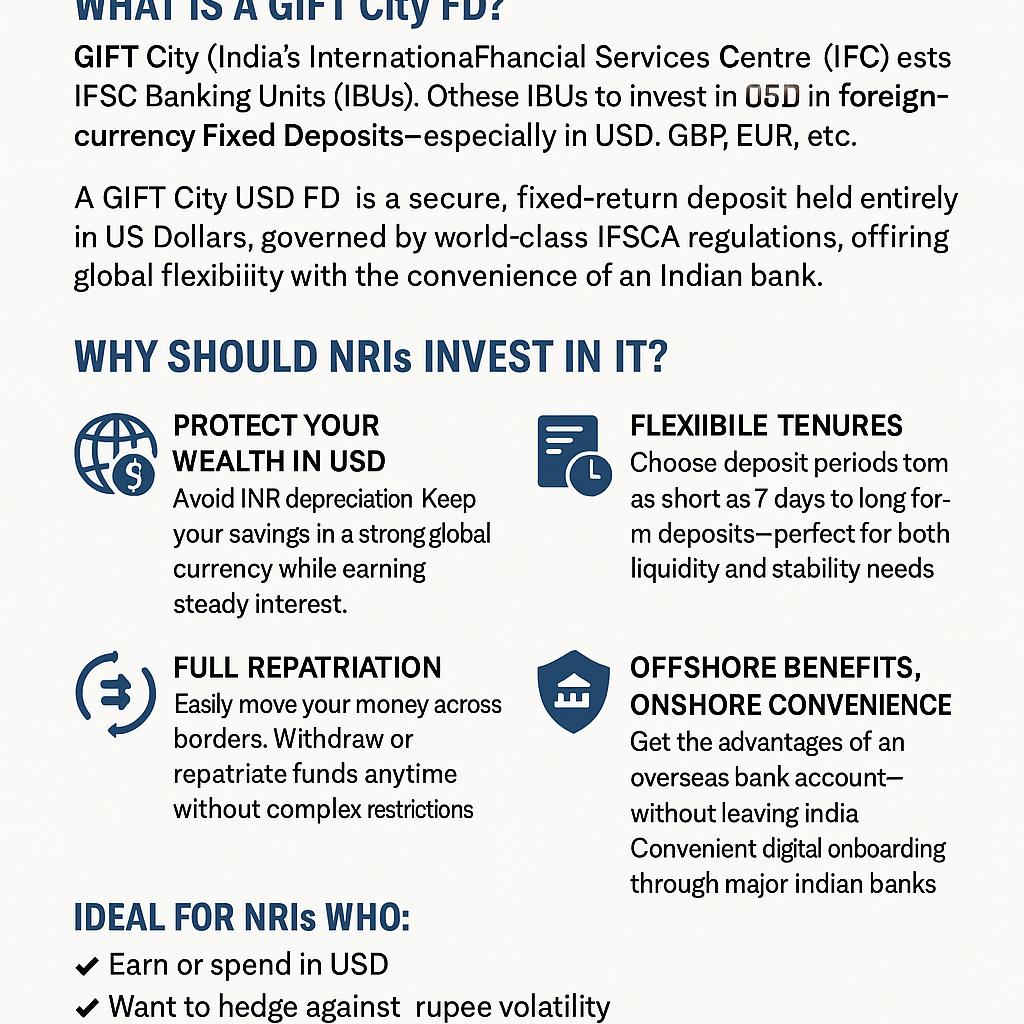

“GIFT City USD FD” refers to a fixed-term deposit (time deposit) offered by a bank’s IBU in GIFT City — denominated in US Dollars (or potentially other foreign currencies). In other words: you deposit USD (or other permitted currency) with the IBU for a fixed period, and earn interest on that deposit.

Key features:

- Foreign-currency deposit: The deposit is in USD (or other globally convertible currencies, depending on bank).

- Flexible tenure: Depending on bank/IBU, the term can start from as short as a few days (e.g. 7 days) to much longer periods (months or years).

- Interest paid in foreign currency: Interest accrues (and is paid) in the same currency — so you stay exposed to USD (or the chosen foreign currency), not Indian Rupees.

- Offshore-like regulatory and tax treatment (within India): Since GIFT IFSC is special-status zone, foreign-currency deposits here enjoy certain regulatory and tax benefits under IFSC rules.

- Repatriability and global convenience: Because the deposits are in foreign currency and managed under IFSC framework, it’s easier for NRIs to repatriate funds (principal + interest), or use them for international transfers.

Thus, GIFT City USD FD is essentially like opening a “foreign-currency fixed deposit account” in an “offshore-style” financial zone — but within India’s regulatory framework.

Who can use GIFT City USD FD (Eligibility)

- Primarily Non-Resident Indians (NRIs) or eligible foreign-residents.

- Some banks may allow resident Indians under certain rules (e.g. under Liberalised Remittance Scheme (LRS) for permitted transactions), but broadly the offering is aimed at NRIs / foreign-currency residents vs. domestic-rupee depositors.

Why GIFT City USD FD — What Makes It Special vs Regular Domestic FDs

- Currency-denomination in USD (or other foreign currency): Avoids rupee-depreciation risk — useful if your income/spending is in foreign currency or you want to hold value in USD.

- Global banking flexibility and cross-border convenience: Easier repatriation, ability to remit internationally, hold foreign-currency savings — helpful for NRIs.

- Regulatory/tax framework under IFSC: Foreign-currency deposits in GIFT IFSC often have favourable tax/treatment compared to on-shore domestic deposits.

- Flexibility in tenure — including short-term or long-term — gives liquidity and investment planning freedom (short-notice withdrawal, or long-term savings).

- Access to multiple currencies: Not limited to USD — many IBUs support GBP, EUR, AUD, CAD etc for both savings/current accounts and term deposits.

What It Is Not / What to Know — Limitations & Conditions

- These are not INR-deposits — you bear currency-exchange risk if you later convert to INR or another currency.

- Tax/residency implications depend on your country of residence: while interest may be exempt/treated differently under IFSC rules (within India), you may have to declare interest income as per laws of the country you live in.

- The regulatory benefits relate to IFSC/SEZ special status — GIFT City USD-FD is managed under offshore-style framework but still subject to Indian regulations (as managed by the IBU under IFSCA & RBI oversight).

- Not all banks/IBUs may have identical features: minimum deposit amounts, currencies offered, tenure flexibility, digital vs manual opening — these vary per bank.

How to Get Started (Typical Steps for a NRI)

- Identify a bank operating an IBU at GIFT IFSC (many major Indian banks and even foreign banks have IBUs).

- Approach the IBU (or use digital banking if the bank supports) to open a foreign-currency account / term deposit account — choose currency (e.g. USD) and tenure.

- Remit foreign currency from abroad (or convert and fund) — deposit the amount as fixed deposit per the bank’s rules.

- On maturity (or per your plan), withdraw or renew, or repatriate principal + interest to your country of residence or use as needed.

You can benefit by placing USD fixed deposits (or other foreign-currency FDs) through GIFT City (via its IFSC-based International Banking Units, IBUs).

Key Benefits of USD FDs via GIFT City for NRIs

• Foreign-currency denomination protects against INR depreciation

- The FDs are denominated in international currencies (e.g. USD). That means you avoid the risk of rupee depreciation reducing your returns when converted to foreign currency.

- This is different from standard INR-denominated deposits, so if you expect to spend or remit money abroad, you preserve value better.

• Flexible tenures (short and long) + ease of withdrawal

- Through GIFT City IBUs, you can often choose FD tenures as short as a week (or a few days) all the way up to several years.

- Many banks allow partial or full premature withdrawal (although with a small penalty in interest).

- This flexibility is more attractive than some of the traditional NRE/FCNR-type FDs which often impose longer minimum tenures.

• Tax-efficient — no TDS in India, and interest may be taxed only in country of residence

- Interest earned on GIFT City FDs is generally not subject to Tax Deducted at Source (TDS) in India.

- Because GIFT City IFSC is treated as an offshore/foreign-currency jurisdiction under Indian regulations, many returns are “outside” the usual Indian domestic-tax regime.

- As an NRI, you’ll likely pay tax (if any) as per the tax laws of your country of residence — which can be beneficial if that jurisdiction has lower tax rates or favourable double-taxation provisions.

• Full repatriation & ease of cross-border banking

- Funds (principal + interest) in GIFT City USD FDs are fully repatriable to your country of residence, without major regulatory hurdles.

- Opening and operating a foreign-currency deposit account via an IBU in GIFT City is straightforward for NRIs.

• Regulated and secure — under international-standard oversight

- GIFT City’s IFSC is regulated by International Financial Services Centres Authority (IFSCA), which oversees banking, funds, and financial services under a unified framework — giving a layer of regulatory protection.

- The offshore-style structure aims to combine convenience of domestic banking with many features of overseas banking — but within India.

Why GIFT City FDs Might Be Preferable to Traditional NRE/FCNR Options

- Traditional NRE/FCNR FDs in India are often INR-linked or have longer mandatory lock-in periods; GIFT City lets you maintain USD (or other currency) deposits directly, with flexible tenures.

- Because there’s no TDS and the deposit is foreign-currency-denominated, you enjoy better “real value preservation” while your funds remain abroad — particularly useful if you earn/spend in dollars or another foreign currency.

- The ability to repatriate funds freely and quickly is valuable if you want easy movement of money between your country of residence and abroad (for spending, investment or retirement).

Important Considerations / What to Check

- Even though interest may be tax-free in India, you must check whether your country of residence taxes foreign-currency interest or foreign-currency income. Global tax/residency rules matter.

- Currency-exchange risk: If you eventually convert USD (or other foreign currency) back to INR (or another currency), exchange-rate fluctuations will affect the rupee value.

- Minimum deposit amounts / KYC: Some banks/IBUs may have requirements such as you having an existing NRE account or certain other documents.

- Regulatory limits: If using outside remittance routes (e.g. LRS) for funding FDs via GIFT City, be aware of applicable limits or reporting / compliance requirements.

In What Situations Investing via GIFT City Makes the Most Sense

If you are an NRI who:

- earns income in USD (or another foreign currency), or expects to spend/retire abroad — GIFT City USD FDs help preserve value;

- wants flexibility in tenure and liquidity rather than long-lock FDs;

- values easy repatriation, minimal compliance hassle in India, and simpler cross-border banking;

- prefers interest and returns that are outside Indian ₹-denominated risk (INR depreciation), and possibly lower Indian-tax obligations;

Then GIFT City’s USD-FD option offers a compelling combination of benefits.

Here’s a mini-comparison of current (or recently published) USD fixed-deposit (FD) interest rates via GIFT City (IFSC/IBU banking) for NRIs — from a few representative banks. Use this to get a sense of what your money might earn depending on the bank and tenure.

Example Current / Recent USD FD Rates at GIFT City (as of late 2025)

| Bank / IBU / Source | Tenure (USD FD) | Approx. Interest Rate (p.a.) / Notes |

|---|---|---|

| ICICI Bank — GIFT City IBU | 7– 30 days | ~ 3.70% ICICI Bank |

| ICICI Bank — GIFT City IBU | 30 days – <3 months | ~ 3.90% p.a. ICICI Bank |

| Axis Bank — GIFT City IBU | 1 week – <1 month | ~ 3.65–3.70% p.a. AxisBank+1 |

| Axis Bank — GIFT City IBU | 1 to <3 months | ~ 3.95–4.00% p.a. AxisBank |

| Axis Bank — GIFT City IBU | 6 to <9 months (and up to 1 year) | ~ 4.00–4.05% p.a. AxisBank+1 |

| Federal Bank — GIFT City IBU (retail) | Recent published rate (retail) | ~ 4.00% p.a. (USD) Federal Bank |

What This Tells You (and What to Watch Out For)

- For short-term USD deposits (weeks to a few months), rates tend to be in the ~3.6% to ~4.0% p.a. range.

- For medium-term horizons (6–12 months), you might get marginally higher — up to ~4.0–4.05% p.a. (at least with Axis Bank, per recent tables).

- Compared to older publicized global-FD rates (or certain standard FDs in INR), these rates are modest — but the key advantage remains currency-denomination in USD (no currency conversion risk while deposit remains in USD), flexible tenures, and repatriability.

- Note: As with any interest-rate product — a few percent points may not fully offset currency exchange risk (if you convert back to INR or another currency later) or inflation.

What to Confirm When You Actually Invest

When you approach a bank for a GIFT City USD FD, make sure to check:

- The exact interest rate for your chosen tenure and deposit amount (rates may vary slightly depending on amount or whether premature withdrawal is allowed).

- The premature withdrawal / partial withdrawal conditions and any penalty (some banks allow digital partial/full withdrawal, but it may reduce interest).

- The minimum deposit amount (some GIFT-City IBUs may require a certain minimum, e.g. USD 1,000 or more).

- Tax/regulatory implications based on where you reside (though returns from GIFT City FDs are often treated as foreign-currency, which may impact taxation differently compared to INR FDs

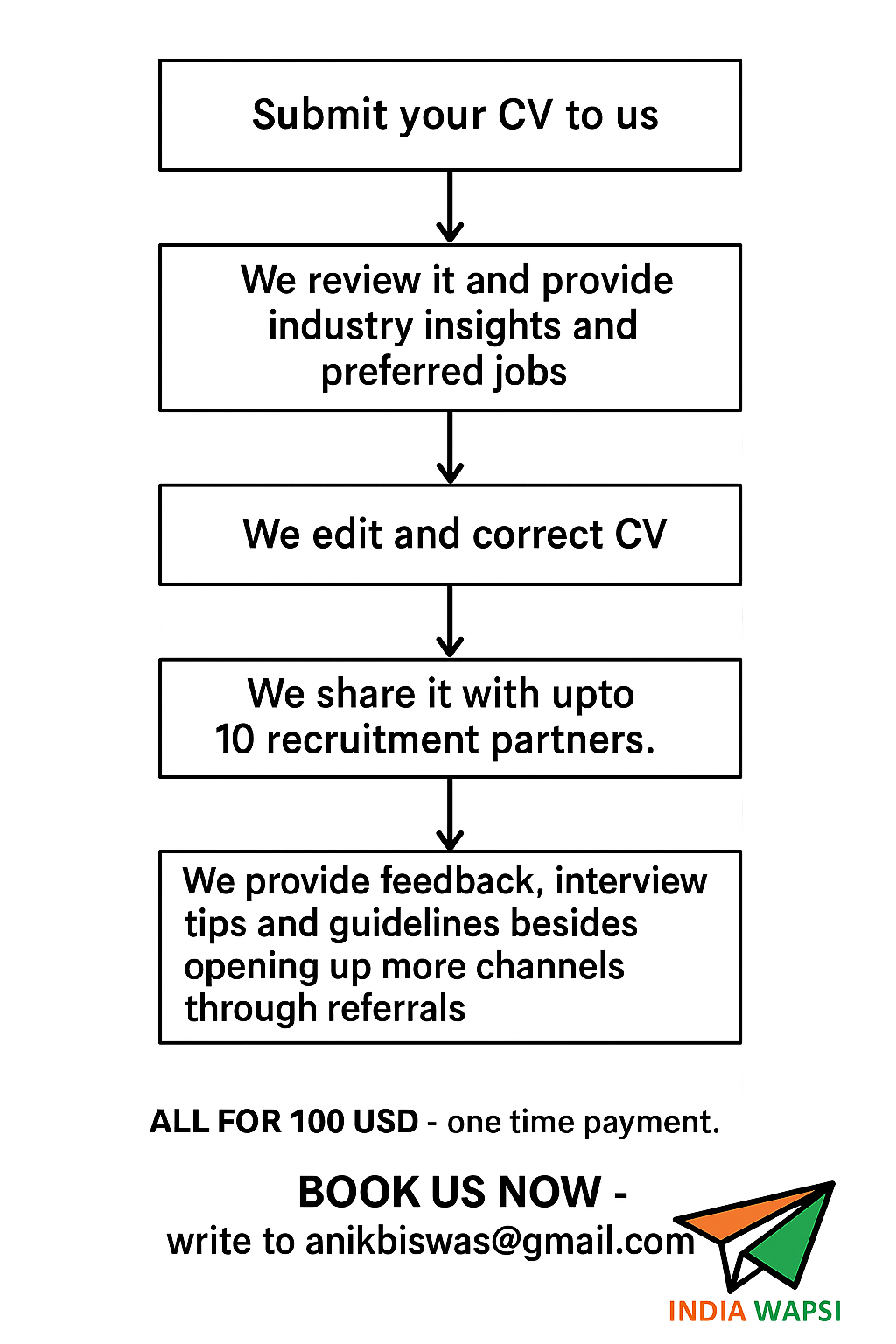

At India Wapsi, we provide you with the best advice on investments for NRIs and returning Indians. Please write to us today and get customized advice for your unique needs, write to us now at anikbiswas@gmail.com.